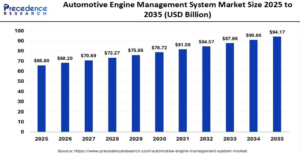

The global automotive engine management system market size was calculated at USD 65.80 billion in 2025 and is predicted to increase from USD 68.20 billion in 2026 to approximately USD 94.17 billion by 2035, expanding at a CAGR of 3.65% from 2026 to 2035. This market is growing due to the implementation of stringent global emissions along with fuel economy standards such as Euro 6/7, BS-VI, and CAFE standards, which are the main drivers forcing OEMs to accept advanced engine management systems for enhanced combustion efficiency.

Automotive Engine Management System Market Key Insights

- North America dominated the global automotive engine management system market in 2025.

- Asia-Pacific is expected to grow at the fastest CAGR between 2026 and 2035.

- By component, the electronic control unit (ECU) segment dominated the market in 2025.

- By component, the sensors segment is expected to expand at the fastest CAGR between 2026 and 2035

- By engine type, the gasoline engines segment held the largest market share in 2025.

- By engine type, the hybrid engines segment is expected to expand rapidly during the forecast period.

- By vehicle type, the passenger cars segment contributed the biggest market share in 2025.

- By vehicle type, the two-wheelers segment is expected to witness significant growth between 2026 and 2035.

Role of AI Automotive Engine Management System Market

Artificial intelligence (AI), specifically machine learning and deep learning , allows engines to adapt to changing conditions in real time. It improves combustion by managing air-fuel ratios, ignition timing, and even fuel injection based on live sensor data, leading to enhancements in fuel efficiency by up to 10%. AI is vital in balancing the power between internal combustion engines and electric motors in hybrid vehicles. It also assists in minimizing toxic emissions such as CO2, NOx, and particulate matter by handling catalytic converters and optimizing exhaust gas recirculation based on driving patterns.

Regional Outlook for Automotive Engine Management System Market

North America held a major revenue share of the market in 2025. This is due to the high concentration of major automakers and suppliers, coupled with robust R&D spending, which drives the rapid development and even adoption of technologies such as gasoline direct injection, cylinder deactivation, and electronic control units. The EPA and CAFE standards in the U.S. mandate remarkable improvements in fuel efficiency and reductions in greenhouse gases, forcing automakers to accept sophisticated AEMS to control combustion, fuel injection, and emissions.

Asia-Pacific is expected to experience the fastest growth during the predicted timeframe, due to the region being a center for two-wheelers, three-wheelers, and passenger cars, mainly in India, enhancing the need for EMS components. High manufacturing output in India, China, and Japan, combined with growing disposable income, boosts the need for advanced vehicle technologies.

Europe is expected to grow at a significant CAGR throughout the forecast period. This is due to the shift towards electric and hybrid vehicles, which demand complex EMS to manage dual power sources, boosting innovation in battery management systems. European automotive players deeply invest over €150 billion annually in R&D and capital projects, aiming for innovation and even technological advancements in vehicle systems.

Market Scope

| Report Coverage | Details |

| Market Size in 2025 | USD 65.80 Billion |

| Market Size in 2026 | USD 68.20 Billion |

| Market Size by 2035 | USD 94.17 Billion |

| Market Growth Rate from 2026 to 2035 | CAGR of 3.65% |

| Dominating Region | North America |

| Fastest Growing Region | Asia Pacific |

| Base Year | 2025 |

| Forecast Period | 2026 to 2035 |

| Segments Covered | Component, Engine Type ,Vehicle Type ,and region |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

Segmental Outlook of Automotive Engine Management System Market

Component Insights

The electronic control unit (ECU) segment registered its dominance in the automotive engine management system market in 2025. This is due to its vital role in enhancing engine performance, maximizing fuel efficiency, and even ensuring compliance with stringent global emission regulations. Modern vehicle architecture is changing toward central or domain ECUs to handle multiple functions, reducing wiring weight and improving data processing speed, mainly for advanced driver assistance systems.

The sensors segment is expected to gain the highest market share between 2026 and 2035. It is driven by strict emission regulations, the need for higher fuel efficiency, and the requirement for real-time engine monitoring. The growth of electric and hybrid vehicles has remarkably boosted the demand for specialized sensors for battery management, thermal management, and thus, regenerative braking.

Engine Type Insights

The gasoline engines segment accounted for the highest automotive engine management system market share in 2025. This is due to its high adoption in passenger cars, lower manufacturing expenses, and better compliance with strict emission regulations (e.g., Euro 6) compared to diesel. The growth of gasoline direct injection (GDI) technology, which enhances efficiency and reduces emissions. Increased acceptance of advanced, fuel-efficient technologies such as turbocharging, gasoline direct injection (GDI), and variable valve timing demands more sophisticated and reliable EMS.

The hybrid engines segment is expected to expand rapidly in the market in the coming years, because innovations in battery technology, electric motors, and regenerative braking systems have enhanced performance, improving the appeal of hybrid vehicles. Increasing knowledge regarding sustainability has boosted the need for eco-friendly vehicles, with hybrids representing a significant section of future vehicle sales.

Vehicle Type Insights

The passenger cars segment led the market in 2025. This is due to high production volumes and strict emission regulations, for e.g., BS VI, China 6, and consumer need for fuel efficiency, improved performance, and advanced, connected features. Governments are enforcing stricter emission standards, thus forcing manufacturers to integrate advanced sensors along with electronic control units to meet compliance.

The two-wheelers segment is expected to show lucrative growth in the upcoming period, due to rapid, strict emission regulation enforcement, such as Bharat Stage VI in India. There is a switch from carburetors to electronic fuel injection along with electronic control units. The massive, growing need for two-wheelers in developing economies, mainly India, China, and Southeast Asia, drives the demand for affordable, compact EMS solutions.

Recent Developments

- In November 2024, Marelli launched its VEC_480, an advanced Electronic Control Unit to support real-time AI applications for motorsport vehicles, enhancing computational performance and enabling complex functions like neural virtual sensors, predictive analysis, and real-time video processing.

- In August 2024, Continental AG declared a potential spinoff of its automotive business, which involves its engine management system operations, to be presented for shareholder approval by April 2025. This strategic move targets to improve focus on software-defined vehicle architectures, thus, integrating the engine management system with advanced driver assistance systems for enhanced vehicle efficiency and safety.

AI Agents Market Companies

Infineon Technologies AG

A leading semiconductor manufacturer specializing in power electronics, automotive chips, and IoT solutions.

The company focuses on enabling energy efficiency, smart mobility, and secure digitalization. Marketplace with over 200 industry-specific agents for productivity and workflow automation.

Sensata Technologies

A global industrial technology company that develops sensors, controls, and sensor-rich solutions.

Its products are widely used in automotive, aerospace, and industrial applications for safety and efficiency. Apple Inc.

Denso Corporation

A major Japanese automotive components manufacturer and a key supplier to global automakers.

It focuses on advanced mobility solutions, including electrification, thermal systems, and autonomous driving technologies.

BorgWarner

A global leader in clean and efficient propulsion systems and technologies.

The company is actively driving the transition toward electric vehicles with innovative electrification solutions.

Hitachi Astemo

A subsidiary of Hitachi focused on advanced mobility solutions, including powertrain, chassis, and safety systems.

It aims to support next-generation vehicles with electrification, autonomous driving, and connected technologies.

{kind=link}