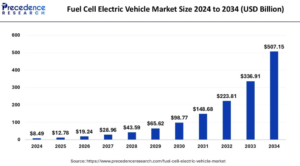

The global fuel cell electric vehicle market size was valued at USD 8.49 billion in 2024 and is projected to reach around USD 507.15 billion by 2034 with a CAGR of 50.53%.

Key Highlights

- In 2024, Asia Pacific led the global market, accounting for a 64% share.

- North America is expected to grow at a significant CAGR during the forecast period.

- The passenger vehicle segment held the largest market share by vehicle type in 2024.

- By range, the short-distance segment dominated the market with the highest share in 2024.

Role of AI in the Fuel Cell Electric Vehicle (FCEV) Market

- Optimized Fuel Cell Performance

AI enhances the efficiency of fuel cell systems by optimizing hydrogen consumption and power output. It helps in balancing energy supply and demand, ensuring better performance and longer fuel cell lifespan. - Predictive Maintenance and Diagnostics

AI-driven predictive analytics monitor vehicle health in real time, detecting potential failures before they occur. This reduces downtime, lowers maintenance costs, and improves vehicle reliability. - Autonomous and Assisted Driving

AI powers advanced driver assistance systems (ADAS) in FCEVs, enabling features such as adaptive cruise control, lane-keeping, and collision avoidance. It also plays a crucial role in self-driving fuel cell vehicles. - Hydrogen Fuel Management

AI helps optimize hydrogen storage, distribution, and refuelling processes. Smart algorithms predict hydrogen demand and assist in efficient refuelling station placement, reducing wait times and enhancing user convenience. - Route Optimization and Energy Efficiency

AI enables real-time route planning based on traffic conditions, terrain, and hydrogen availability. This ensures maximum energy efficiency and extends the driving range of FCEVs. - Battery and Energy Management Systems

AI-driven systems manage energy distribution between the fuel cell stack and onboard batteries, optimizing power delivery based on driving conditions. This enhances performance and extends battery life. - Enhanced User Experience

AI-powered infotainment and in-vehicle assistants improve driver and passenger experience through voice commands, navigation support, and personalized driving recommendations. - Sustainability and Emissions Monitoring

AI helps track and optimize hydrogen production processes, ensuring they remain environmentally friendly. It also monitors emissions, ensuring compliance with regulatory standards.

Regional Outlook of the Fuel Cell Electric Vehicle (FCEV) Market

Asia Pacific

- Largest Market: Asia Pacific is currently the largest market for FCEVs.

- Market Size: Estimated at USD 5.43 billion in 2024. Projected to reach around USD 327.11 billion by 2034.

- CAGR: Expected to grow at a CAGR of 50.66% from 2025 to 2034.

- Driving Factors:

- Stringent government policies aimed at curbing pollution levels and banning diesel engines.

- Policies in place to promote the adoption of FCEVs.

- Planned construction of 1000 refuelling stations across the region by 2032 to meet industry demand.

- Major players like Hyundai Motor Company and Toyota Motor Company are offering FCEVs (cars, buses, and logistical vehicles) in the region.

- Rapid industrialization and expansion of production facilities.

- Japan’s declaration of being carbon neutral by 2050.

- Increasing government investments in infrastructure for electric vehicles.

Fuel Cell Electric Vehicle (FCEV) Overview

The fuel cell electric vehicle (FCEV) market is experiencing significant growth due to rising environmental concerns, advancements in hydrogen fuel cell technology, and government incentives promoting zero-emission vehicles. FCEVs utilize hydrogen as a fuel source, generating electricity through a fuel cell stack to power the vehicle, emitting only water as a byproduct.

Major automakers, including Toyota, Hyundai, and Honda, are investing heavily in FCEV development, making them a viable alternative to traditional internal combustion engine (ICE) vehicles and battery electric vehicles (BEVs).

Market Drivers

Stringent Emission Regulations – Governments worldwide are enforcing stricter emission norms to combat climate change, encouraging the adoption of hydrogen-powered FCEVs.

Growing Demand for Zero-Emission Vehicles – Increasing awareness of sustainability and carbon reduction is pushing industries and consumers toward fuel cell technology.

Advancements in Hydrogen Infrastructure – Expanding hydrogen refueling networks, particularly in countries like Japan, South Korea, Germany, and the U.S., are supporting FCEV adoption.

Longer Range and Faster Refuelling – Compared to BEVs, FCEVs offer a longer driving range and faster refuelling times, making them attractive for commercial fleets and long-haul transportation.

Government Incentives and Investments – Subsidies, tax credits, and funding for hydrogen production and fuel cell technology research are boosting market growth.

Market Opportunities

Expansion of Hydrogen Production – Increased investment in green hydrogen production through renewable sources can further drive FCEV adoption.

Growth in Heavy-Duty and Commercial Vehicles – Hydrogen-powered buses, trucks, and trains are gaining traction as viable solutions for reducing emissions in freight and public transport.

Integration with Renewable Energy – Utilizing excess renewable energy for hydrogen production can enhance energy sustainability and grid stability.

Technological Innovations in Fuel Cell Efficiency – Continuous advancements in fuel cell durability, efficiency, and cost reduction will make FCEVs more competitive in the coming years.

Developing Markets in Asia-Pacific and Europe – Countries like China, South Korea, and Germany are heavily investing in hydrogen fuel infrastructure, creating new market growth opportunities.

Market Challenges

High Cost of Fuel Cell Technology – Despite advancements, FCEVs remain expensive due to costly fuel cell components and hydrogen storage technology.

Limited Hydrogen Refuelling Infrastructure – A lack of widespread hydrogen stations restricts FCEV adoption, particularly in developing regions.

Energy Efficiency Concerns – Hydrogen production, storage, and transportation involve energy losses, making the overall efficiency lower compared to direct battery-powered EVs.

Competition from Battery Electric Vehicles (BEVs) – The growing adoption of BEVs, supported by expanding charging networks, presents a challenge to the FCEV market.

Safety and Public Perception – Handling and storing hydrogen involve safety risks, and consumer awareness of FCEV benefits remains relatively low.

Recent Development

- In September 2024, BMW announced the launch of its first-ever series production hydrogen-powered fuel cell electric vehicle (FCEV) in 2028.

- In October 2024, Hyundai announced the launch of INITIUM hydrogen fuel cell electric vehicle (FCEV) concept at its ‘Clearly Committed’ event held at Hyundai Motor studio Go yang.

Fuel Cell Electric Vehicle Market Companies

- Audi AG

- Ballard Power systems Inc.

- BMW Group

- Daimler AG

- Honda Motor Co limited

- Volvo group

- Toyota Motor Corporation

- General Motors company

- Man Se

- American Honda Motor Co.

- Toshiba

Segments Covered in the Report

By Vehicle

- Passenger Vehicles

- Light commercial vehicles

- Bus

- Trucks

- Heavy Duty Vehicles

- Agriculture

- Automotive

- Others

By Range

- Short Range

- Long Range

By Geography

- North America

- U.S.

- Canada

- Europe

- U.K.

- Germany

- France

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Malaysia

- Philippines

- Latin America

- Brazil

- Rest of Latin America

- Middle East & Africa (MEA)

- GCC

- North Africa

- South Africa

- Rest of the Middle East & Africa

{kind=link}