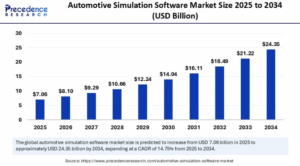

According to Precedence Research, the global automotive simulation software market size is expected to reach around USD 24.35 billion by 2034 from USD 6.15 billion in 2024, growing at a CAGR of 14.75%.

With complexity in modern vehicles and stringent safety regulations, simulation tools enable effective design, testing, and validation, minimizing time and cost for manufacturers while accelerating innovation.

Automotive Simulation Software Market Key Highlights

- The global market is expected to climb from USD 7.06 billion in 2025 to USD 24.35 billion by 2034.

- North America dominates with a 34% share in 2024, and the USA alone is projected at USD 5.92 billion by 2034.

- Asia Pacific will grow fastest at a 15.80% CAGR.

- Structural simulation contributed about 24% of the market in 2024.

- Passenger vehicles accounted for 46% of market share in 2024, while electric vehicles are projected to outpace growth at 19.60% CAGR.

- On-premises solutions held a larger share (55% in 2024), while cloud-based platforms are growing rapidly at 18.40% CAGR.

- Major segments: Simulation type, development mode, application, vehicle type, component, technology, software, service, and region.

Revenue Table Breakdown

| Year | Global Market Value (USD Billion) |

|---|---|

| 2024 | 6.15 |

| 2025 | 7.06 |

| 2034 | 24.35 |

| Region | Market Share (%) | 2024 Value (USD Billion) |

|---|---|---|

| North America | 34% | 1.46 |

How Artificial Intelligence is Shaping Automotive Simulation

AI is becoming integral to automotive simulation by generating 3D environments, automating scenario creation, and modeling complex systems. These advancements, implemented in platforms like SCANeR, improve realism and accuracy while reducing engineers’ workloads.

AI also analyzes driving patterns in real-time, boosting road safety and fueling smarter production processes. Use cases span digital twins, ADAS/autonomous driving simulation, supply chain optimization, and improved customer support—making automotive design faster, safer, and more efficient.

Market Growth Factors

What is Fueling Market Expansion?

Major drivers include heightened complexity in vehicle systems, integration of electronic control units (ECUs), and the rollout of advanced driver assistance systems (ADAS) and infotainment platforms. The move to cloud-based simulation offers scalability and flexibility, a boon for manufacturers adapting to new regulations and consumer expectations.

Is the Future Electric and Autonomous?

The rise of electrification, battery simulation, and autonomous systems is fundamental to growth. Simulation accelerates time-to-market, enhances vehicle safety features, and curtails costs by enabling virtual prototype testing.

Opportunities & Trends: Is Innovation Outpacing Regulation?

Cloud-Based Platforms: Accessibility Versus Control

Cloud-based simulation platforms deliver unprecedented accessibility, allowing engineers and researchers to use infrastructure, platforms, and software as an on-demand service removing the IT friction of traditional deployments.

These platforms enable faster deployment, easier scaling, and improved performance at reduced IT costs.

However, shifting to the cloud may mean less direct control over infrastructure compared to on-premises solutions, which still offer greater security and oversight but require higher maintenance and capital investment.

Cloud-based simulation also supports rapid innovation by making powerful modeling tools available anywhere and enabling real-time collaboration across global teams.

AI-Driven Design: Unlocking Hyper-Efficient Prototyping

AI-powered design automation is revolutionizing automotive simulation by generating complex 3D environments, automating scenario creation, and creating high-fidelity surrogate models for validation.

Machine learning-driven simulation software can auto-generate thousands of design options, learn from patterns in synthetic data, and detect anomalies, all accelerating prototyping cycles and improving predictive validation for vehicle safety and performance.

These advancements help manufacturers minimize physical prototyping, gain deeper insight into system behaviours, and deliver innovative vehicles faster to market.

Sustainable Mobility: Fast-Tracking Eco-Friendly EVs

Simulation is pivotal in developing sustainable, electric vehicles by enabling fault simulation, design optimization, compliance testing, and thermal management for battery packs .

Automakers leverage multiphysics simulation to streamline EV battery production, reduce costs, cut fault rates, and navigate complex safety standards for new models.

These capabilities speed up product launches and help meet growing regulatory demands for cleaner, greener vehicles in an increasingly electrified market.

Digital Twins: Enabling Smart Mobility Across Regions

Virtual vehicle twins digital replicas of real-world vehicles empower manufacturers to shift rapidly towards smart mobility by modeling, testing, and refining designs in virtual environments.

Digital twins facilitate real-time monitoring, predictive maintenance, and continuous improvement across the vehicle lifecycle, enhancing both product reliability and user experience with minimal physical intervention.

Regional & Segmentation Analysis

North America: Market Leader at 34% Share

North America currently holds the largest market share of about 34% in the automotive simulation software market.

This leadership is largely due to rapid advancements and early adoption in autonomous vehicle technology, electric vehicles (EVs), and sophisticated driver assistance systems (ADAS).

The presence of major automotive OEMs, technology developers, and stringent safety and emission regulations encourage extensive simulation usage for safe, compliant, and efficient vehicle design.

Significant investments in R&D and cloud-based platforms also support North America’s dominant position.

Asia Pacific: Fastest Growing Region

Asia Pacific is projected to witness the highest compound annual growth rate (CAGR) of approximately 15.8%, attributed to rapid digital transformation and expanding automotive manufacturing hubs in China, Japan, South Korea, and India.

The region experiences growing demand for electric and hybrid vehicles with increased government incentives for sustainable mobility solutions.

Automotive simulation adoption is rising due to cost efficiency and fast prototyping needs in emerging markets, supported by expanding cloud infrastructure and AI-driven design adoption.

Segmentation Overview

- Simulation Type: Includes structural simulation dominating with about 24% share, thermal, fluid dynamics, electrical component simulation, and multi-physics simulation tools.

- Application: Includes vehicle design & development, battery simulation, ADAS/autonomous driving, manufacturing process simulation, and infotainment systems.

- Component Simulated: Structural components, engine, transmission, brakes, battery, and electronic control units (ECUs).

- Technology: Traditional on-premises simulation solutions account for roughly 55% market share, while cloud-based platforms are rapidly growing with an 18.4% CAGR.

- Software/Service Type: Encompasses standalone simulation software, integrated CAE tools, testing and validation services, and ongoing consulting services.

- End-User: Majorly automotive OEMs, tier-1 suppliers, and research institutes leveraging simulation for faster and safer vehicle development.

- Geographical Regions: North America, Europe, Asia Pacific, Latin America, and Middle East & Africa.

Key Segments and Growth Trajectories

- Passenger Vehicles: Represent the largest application segment with about 46% market share, fueled by demand for innovative safety and infotainment features.

- On-Premises Deployment: Currently dominates market deployment types due to better security and control, holding a major 55% share.

- Structural Simulation: Leading simulation type with significant usage in chassis and body design, contributing approximately 24% share of the simulation type segment.

- Emerging Trends: Cloud-based solutions, AI/ML integrated simulations, and simulations tailored for electric vehicles show the fastest growth, reflecting industry trends towards more flexible, scalable, and intelligent development platforms.

Recent Breakthroughs & Leading Companies

Latest Breakthroughs

- Real-time 3D simulation solutions with adaptive, cloud-based infrastructures.

- Integrated thermal management systems for battery packs widening EV adoption.

- AI/ML feedback loops generating synthetic data and driving innovation in component design.

Leading Companies

- Gamma Technologies: Multi-domain vehicle and powertrain system simulation.

- ESI Group: Virtual prototyping for design, safety, and manufacturing.

- dSPACE: Real-time testing tools for ECUs and vehicle systems.

- Design Simulation Technologies: Simulation tools for mechanical and automotive engineering.

- Dassault Systèmes: Advanced 3D design and full vehicle simulation.

- AVL List: Powertrain, engine, and vehicle system modeling.

- Autodesk: 3D CAD, design optimization, and prototyping.

- Anthony Best Dynamics: Simulation and physical testing for vehicle dynamics.

- Ansys: Multiphysics modeling for safety, durability, and electronics.

- Altair Engineering: Optimization and simulation-driven lightweighting.

Challenges & Cost Pressures

What are the Cost Barriers Facing Automotive Simulation?

High development costs, complexity of simulation tools, and infrastructure maintenance remain top pressures. Making sense of vast simulation data takes time, and critical simulations still struggle to meet high-accuracy standards needed for key safety systems.

Case Study: Synopsys–Ansys Merger – Redefining Simulation and Design in Automotive

Background

- Synopsys Inc. is a global leader in electronic design automation (EDA), specializing in chip design, verification, and semiconductor IP.

- Ansys Inc. is a world-class provider of multiphysics simulation software, covering structural, fluid dynamics, thermal, and electromagnetic domains.

- Both companies had been operating in complementary areas—Synopsys in chip/system design and Ansys in physical-world simulation.

This merger, finalized in September 2025 for $35 billion, is regarded as one of the largest tech acquisitions in engineering software history.

The Strategic Rationale

The motivation behind this deal was simple but powerful: unify digital design and physical simulation into one integrated platform.

- Bridging the Gap

Traditionally, semiconductor engineers use Synopsys tools to design chips, while automotive and aerospace engineers use Ansys to simulate real-world conditions. By merging, they aim to shorten the gap between digital design (EDA) and physical validation (CAE). - AI-Driven Integration

Both companies are investing heavily in AI-powered automation. The unified platform will allow machine learning models to analyze both design and simulation data, delivering predictive insights and automated design recommendations. - Market Expansion

While Synopsys dominates in semiconductors, Ansys has strongholds in automotive, aerospace, industrial manufacturing, and energy sectors. The merger enables cross-selling and entry into each other’s established markets.

Impact on Automotive Simulation Software

For the automotive industry, this merger is particularly significant:

- EV Battery & Powertrain Design

- Ansys tools already simulate battery thermal management, crash safety, and aerodynamics.

- Synopsys brings chip-level design for battery management systems (BMS), AI-based energy efficiency, and power electronics.

- Together, they can create digital twins of EVs—from the chip that manages energy flow to the simulation of battery performance under real-world conditions.

- ADAS & Autonomous Systems

- Synopsys’ strength in AI-driven chips and perception systems integrates with Ansys’ sensor simulation tools (lidar, radar, camera).

- This enables faster and safer virtual validation of autonomous driving functions, reducing reliance on costly physical test miles.

- Vehicle Safety & Reliability

- Multiphysics simulation of mechanical stress, thermal loads, and electromagnetic interference (from Ansys) can be linked with chip-level failure analysis (from Synopsys).

- OEMs gain an end-to-end view of system reliability, from silicon to system.

- Regulatory Compliance

- Automotive OEMs face stringent safety standards (ISO 26262, UNECE ADAS regulations).

- The integrated workflow promises faster regulatory validation by linking design, verification, and simulation datasets.

Integration Roadmap (2025–2026)

- Late 2025: Deal closure and regulatory approvals secured (including final approval from Chinese regulators).

- Early 2026: Launch of the first integrated toolchains combining Synopsys EDA with Ansys multiphysics modules.

- By 2027: Full deployment of a cloud-native simulation-design platform, allowing OEMs and Tier-1 suppliers to co-develop hardware/software systems in one ecosystem.

Expected Benefits for Automotive OEMs & Tier-1s

- Reduced Time-to-Market: Unified design and simulation cut development cycles for EVs and ADAS systems.

- Lower Costs: Virtual prototyping minimizes the need for physical prototypes, saving millions in R&D.

- Improved Accuracy: Linking chip-level EDA with full-vehicle simulation reduces risk of late-stage design flaws.

- Faster Innovation: AI-driven workflows enable rapid exploration of design trade-offs.

- Scalability: Cloud-based integration allows global teams to collaborate in real time.

Market Implications

- Competitive Edge: Synopsys+Ansys sets a new benchmark, challenging Dassault Systèmes, Siemens, and Cadence in the automotive simulation space.

- Customer Base Expansion: Automotive players using Ansys will now be exposed to Synopsys’ silicon design ecosystem vital for next-gen EVs and autonomous vehicles.

- AI & Cloud Shift: The deal accelerates the industry shift toward AI-driven, cloud-based digital engineering ecosystems.

The Synopsys–Ansys merger is not just a financial transaction but a transformative case study in the evolution of automotive simulation software. It exemplifies how uniting EDA, multiphysics, and AI will reshape the way EVs, autonomous systems, and safety-critical components are designed and validated in the coming decade.

{kind=link}